© Export Finance Australia

The views expressed in World Risk Developments represent those of Export Finance Australia at the time of publication and are subject to change. They do not represent the views of the Australian Government. The information in this report is published for general information only and does not comprise advice or a recommendation of any kind. While Export Finance Australia endeavours to ensure this information is accurate and current at the time of publication, Export Finance Australia makes no representation or warranty as to its reliability, accuracy or completeness. To the maximum extent permitted by law, Export Finance Australia will not be liable to you or any other person for any loss or damage suffered or incurred by any person arising from any act, or failure to act, on the basis of any information or opinions contained in this report.

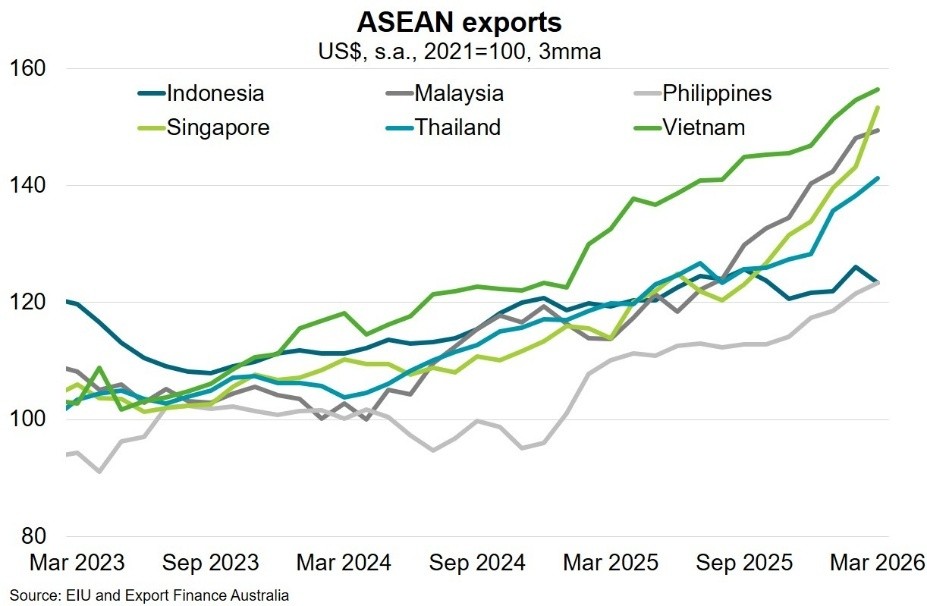

Southeast Asia—Tech exports shield from conflict fallout

The accelerating global boom in Artificial Intelligence (AI) capability and infrastructure investment has sustained strong growth in ASEAN’s electronics-led economies. While almost all ASEAN economies recorded double-digit export growth in Q1 2026, economies integrated into advanced technology value chains outperformed, including Malaysia, Singapore and Vietnam (Chart). Continued strong trade data from Taiwan and South Korea—upstream producers of the electronics supply chain—suggests that AI demand will continue to boost trade performance among downstream ASEAN producers throughout this year.

However, conflict in the Middle East will impose significant economic damage given ASEAN’s heavy dependence on imported energy. Higher energy costs weigh on private consumption and investment and raise production costs across the economy. Thailand and the Philippines are particularly exposed given high energy-import intensity and direct pass-through to consumer prices. Indeed, inflation in the Philippines jumped to 7.2% in the year to April while GDP growth slowed to 2.8% in Q1 2026, the lowest since the pandemic. Other ASEAN governments—including Malaysia and Indonesia—have implemented domestic fuel subsidies that will shield consumers, but increase the burn on public finances. In any case, prolonged disruptions could cause outright energy shortages, especially in countries with limited stockpiles.

Transmission channels extend beyond energy. Shortages could extend to other commodities, including petrochemicals and fertilisers, and affect domestic harvests. ASEAN economies are also exposed via remittances, investment and tourism from the Middle East. Higher bond yields, currency depreciation and higher risk premia magnify the impact of the shock. Though economies with stronger external positions and firmer policy credibility—Malaysia and Singapore—have outperformed in this regard. Downside risks to the regional outlook relate mainly to the duration and severity of the war, however the threat of new US tariffs is an additional driver of uncertainty, while increased economic hardship could invoke increased political and social unrest.