© Export Finance Australia

The views expressed in World Risk Developments represent those of Export Finance Australia at the time of publication and are subject to change. They do not represent the views of the Australian Government. The information in this report is published for general information only and does not comprise advice or a recommendation of any kind. While Export Finance Australia endeavours to ensure this information is accurate and current at the time of publication, Export Finance Australia makes no representation or warranty as to its reliability, accuracy or completeness. To the maximum extent permitted by law, Export Finance Australia will not be liable to you or any other person for any loss or damage suffered or incurred by any person arising from any act, or failure to act, on the basis of any information or opinions contained in this report.

World—Conflict strains economic resilience

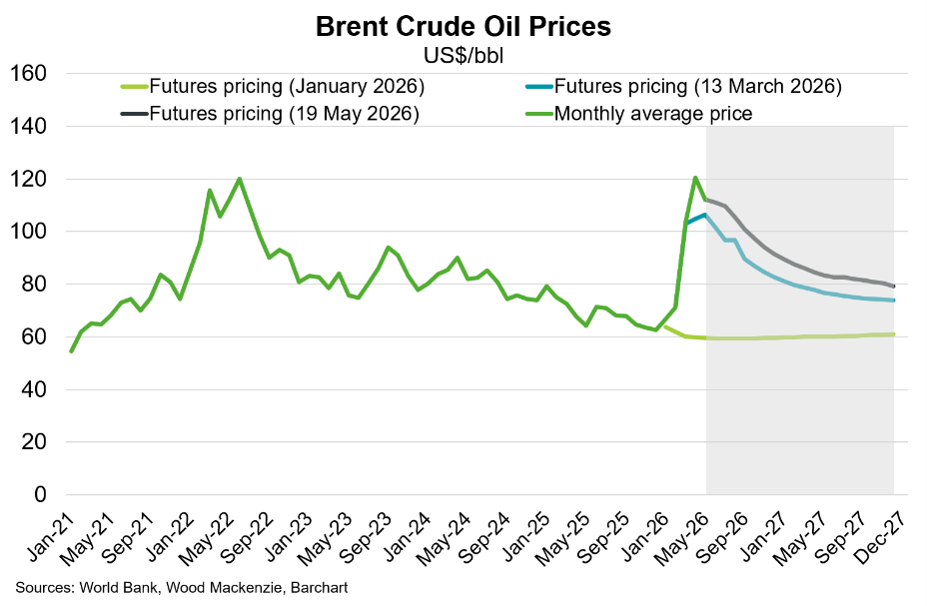

Global economic performance remained resilient into early 2026, supported by an Artificial Intelligence (AI) investment boom, strong asset prices and firm US consumer spending. However, the US-Israeli war with Iran that began over 12 weeks ago has upended the global outlook. Oil supply losses from the Strait of Hormuz are unprecedented; exceeding 1 billion barrels, or 12.8 mb/d since February (around 12% of daily flows), according to the International Energy Agency (IEA). Producers outside the Middle East have lifted exports to record levels, while global oil demand is contracting, particularly for petrochemicals and aviation. Still, global oil inventories are depleting at a record pace; by 250 million barrels over March and April. Even assuming a diplomatic breakthrough allows flows through the Strait of Hormuz to gradually resume from Q3 2026, the IEA expects the oil market to remain in a supply deficit until the end of the year given production will take time to recover. The shock extends to tighter gas, fertiliser, sulfur and helium markets, with higher shipping and insurance costs, higher bond yields and wider credit spreads increasing the drag.

The IMF’s baseline forecast released 13 April assumed that exports from the Middle East normalise by mid-2026, aligning with futures pricing in mid-March. However, oil price expectations have since increased (Chart) and the IMF’s “adverse scenario”—which assumes energy prices remain elevated in 2026, inflation expectations increase and financial conditions tighten—is increasingly likely. This would see global economic growth fall from 3.4% in 2025 to 2.5% in 2026, while inflation increases to 5.4%. Indeed, prolonged closure of the Strait could see a shift from higher prices to widespread constraints that invoke fuel rationing, industrial shutdowns and global stagflation—weak economic activity combined with high inflation. Other risks to the global economic outlook stem from disruptive trade diversion from more protectionist policies, and a repricing of borrowing costs triggered by fiscal vulnerabilities or a revaluation of AI-driven profitability expectations.