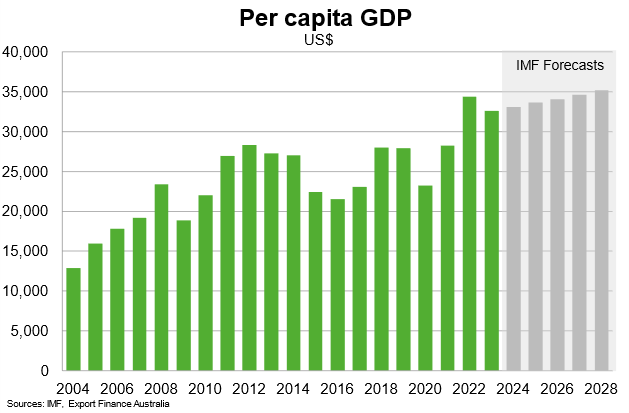

According to IMF estimates, GDP per capita is poised to increase steadily from around US$33,000 in 2023 to US$35,000 in 2028. Saudi Arabia benefits from strong oil-linked growth but suffers from social inequality and relatively high youth unemployment. The expansion of non-oil sectors, including increased public construction and development of new industries, should support higher incomes and reduce inequality over time.

Saudi Arabia

Jump to a section of the page

Saudi Arabia

Last updated: January 2024

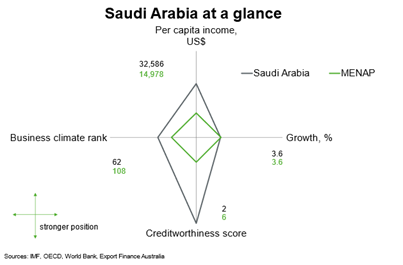

Saudi Arabia is the largest economy in the Middle East, North Africa and Pakistan (MENAP) region, and the world’s largest exporter of oil. Saudi Arabia outperforms most of the MENAP region on per capita income, creditworthiness and ease of doing business while growth is in line with regional peers. The reliance on oil to drive output, jobs and public and external revenue leaves the country vulnerable to swings in oil production, demand, prices and future energy trends. Saudi Arabia remains committed to implementing reforms to diversify its economy away from oil through its Vision 2030 Program.

This chart is a cobweb diagram showing how a country measures up on four important dimensions of economic performance—per capita income, annual GDP growth, business climate and creditworthiness. Per capita income is in current US dollars. Annual GDP growth is the five-year average forecast between 2024 and 2028. Business climate is measured by the World Bank’s 2019 Ease of Doing Business ranking of 190 countries. Creditworthiness attempts to measure a country's ability to honour its external debt obligations and is measured by its OECD country credit risk rating. The chart shows not only how a country performs on the four dimensions, but how it measures up against other regional countries.

Economic outlook

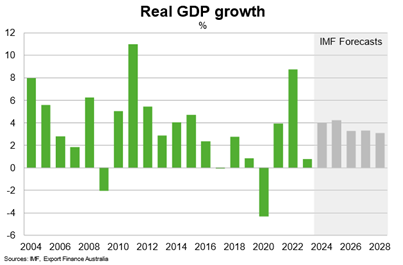

Saudi Arabia’s real GDP growth decelerated to 0.8% in 2023, from 8.7% in 2022 on the back of cuts in oil production and lower oil prices. Non-oil sectors supported growth, underpinned by investments related to the Vision 2030 Program. For example, the tourism recovery benefitted from cultural factors and entertainment initiatives, providing a boost to hospitality. Unemployment also declined, supporting private consumption.

Continued momentum in non-oil sectors will likely support a pickup in real GDP growth to 4% in 2024, as per IMF forecasts. Market expectations suggest Saudi Arabia oil production will marginally increase in 2024, which will support growth. Continued labour market reforms bolster the outlook for consumption, particularly by supporting greater youth and gender equality in employment.

Risks are tilted to the downside. A sharper global economic downturn, lower energy demand and potential falls in oil prices would lower GDP growth. Geopolitical tensions pose broader risks to energy markets and Saudi Arabia’s economic performance. On the upside, higher public investment could support faster growth, but also raise fiscal vulnerabilities.

Saudi Arabia’s long-term outlook is strong. Growth is expected to average 3.5% between 2025 and 2028, as non-oil growth settles. Public construction activity related to Vision 2030 development projects and increasing tourism supports growth in the non-oil sector. Vision 2030 also aims to promote stronger FDI inflows and diversification into higher-value-added industries. The authorities have taken important steps to improve the regulatory and business climate, attract foreign investment and boost private sector participation in the economy. Maintaining long-term growth relies on sustaining reform momentum. Given untapped mineral reserves at an estimated US$2.5 trillion, Saudi Arabia aims to increase foreign investment inflows to develop renewables, which if this is realised, would support long term sustainable growth.

Country risk

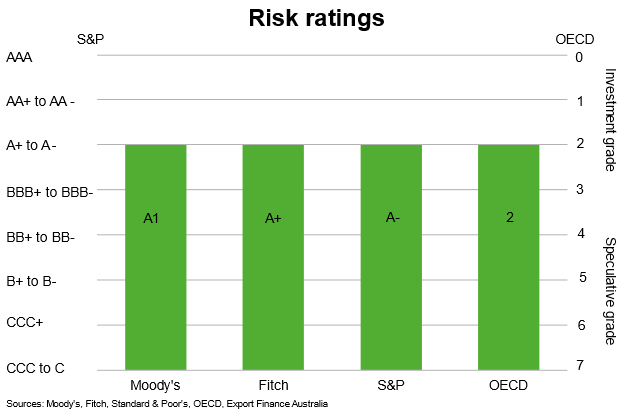

Country risk in Saudi Arabia is low. The OECD country risk rating is 2 and the country has investment grade ratings from all three major private rating agencies. This suggests that there is a low likelihood of the country being unable/unwilling to meet its external debt obligations.

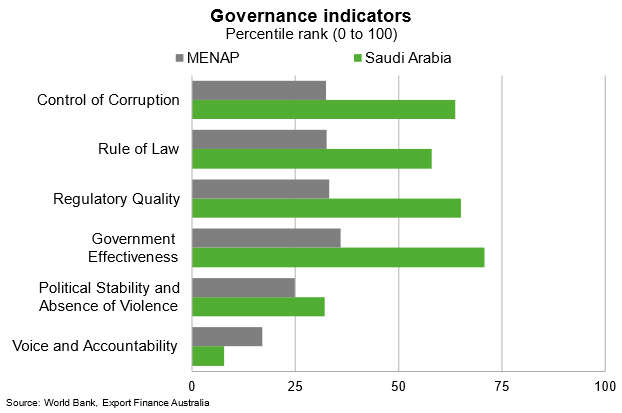

Saudi Arabia scores in the top half of most governance indicators and has a track record of solid fiscal and economic management. That said, Saudi Arabia scores lowly on measures of voice and accountability. The monarchy heads the government, and most laws are based on conservative principles, often limiting freedom of expression.

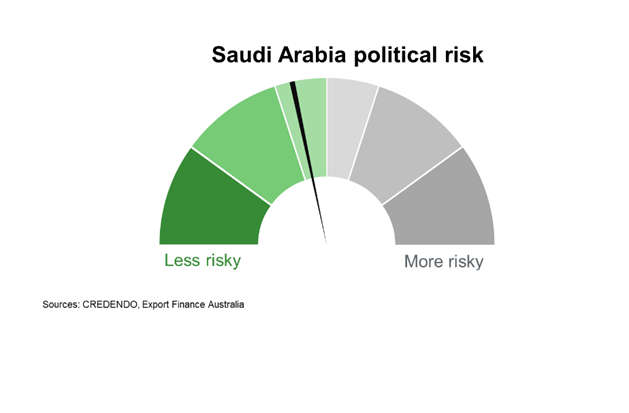

Political risk in Saudi Arabia is low to moderate and includes risks related to the escalation of regional geopolitical tensions that can hinder oil production, investment in non-oil sectors and foreign trade.

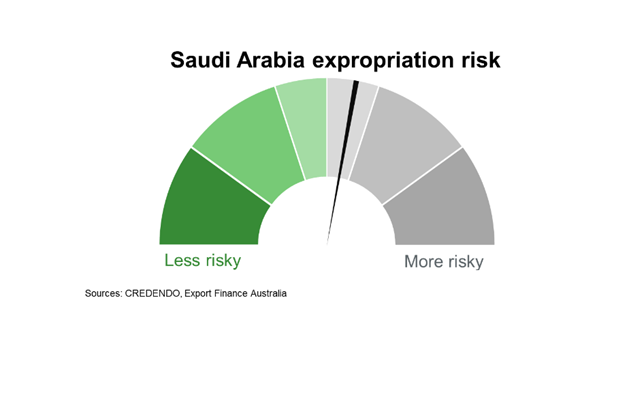

The risk of expropriation in Saudi Arabia is moderate. The US investment climate statements note that generally the Saudi Board of Grievances has jurisdiction over commercial disputes between the government and private contractors. The US is not aware of any cases of foreign investor expropriation without adequate compensation, but some small and medium enterprises have had their investment licences cancelled without justification, causing them to forfeit their investments.

Bilateral relations

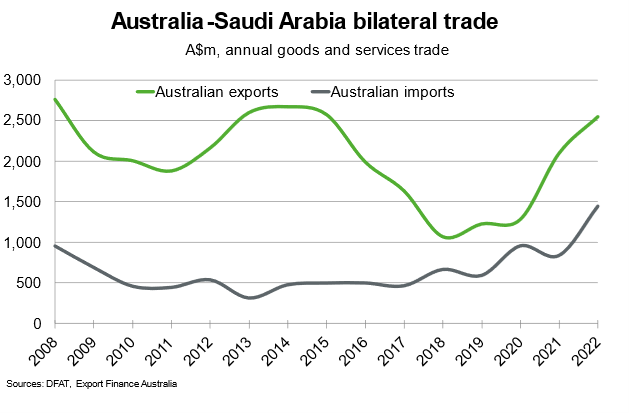

Saudi Arabia was Australia’s 32nd largest trading partner in 2022. Total goods and services trade amounted to $4 billion in 2022. Australia’s major exports to Saudi Arabia in 2022 included barley, meat and education-related travel. Major imports from Saudi Arabia included fertilisers, inorganic chemical elements and road motor vehicles.

There is scope for Australian firms to boost agricultural exports to Saudi Arabia, particularly as the expanding middle class there starts to demand higher-quality proteins and grains. Opportunities also exist in the extractive industries, infrastructure and education and health.

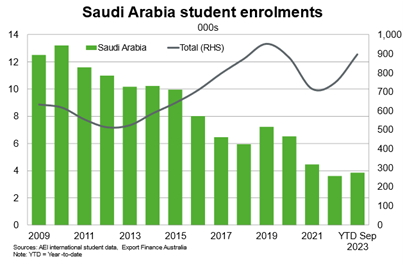

Education dominates Australia’s services exports to Saudi Arabia. Although enrolments in Australian educational institutions have been falling over the past ten years, Saudi students represent the largest cohort from the Middle East region. Saudi Arabia’s Vision 2030 program could provide opportunities for Australian institutions to provide education services in Saudi Arabia. Saudi Arabian scholarship programs can also foster more Saudi students to undertake tertiary studies abroad, including in Australia.

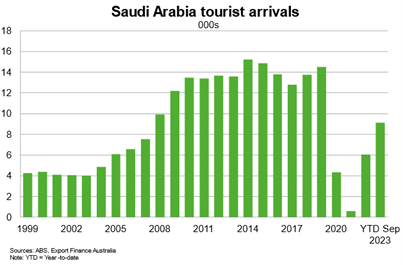

Tourist arrivals picked up further in 2023, reflecting the lifting of travel restrictions and greater international travel. Lower unemployment rates and rising incomes are also supporting Saudi demand for overseas travel. That said, tourist arrivals remain below pre-pandemic levels. A competitive Australian dollar and another year of recovery in international travel should support further demand for Australian tourism, and broader services exports, in 2024.

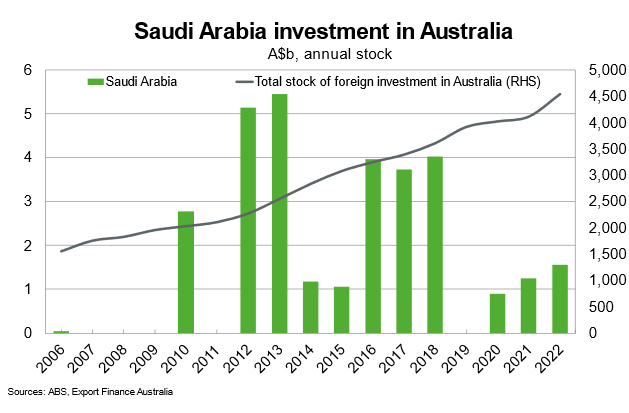

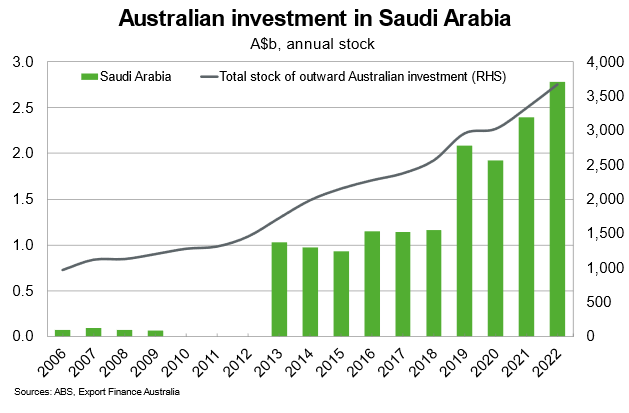

Bilateral investment between Saudi Arabia and Australia is modest. Major Saudi sovereign wealth funds are increasing their international investments, particularly in lithium mining to support energy transition. The Saudi Agriculture and Livestock Investment Company invested in Australian agricultural land in 2019 and is exploring further agriculture investment. Australian investment in Saudi Arabia has been supported by the Vision 2030 program, including projects such as EV Metals Group’s US$3 billion planned investment into lithium processing. Investment also benefits from the Australian Saudi Business Forum, which has already connected more than 150 Australian business members to Saudi Arabia. Further opportunities are likely in the renewables sector.

Useful links

Department of Foreign Affairs and Trade

Austrade